Call Now: 954-554-5103

What is Medicare Advantage

A Medicare Advantage Plan is also known as Medicare Part C. An Advantage Plan will provide you with an alternative to traditional Medicare. These “bundled” plans include Part A, Part B, and usually Part D. With a Medicare Advantage Plan, you will have lower out-of-pocket costs than with just Original Medicare. Also most plans offer extra benefits such as hearing, dental, and vision. In addition, Medicare Advantage Plans focus on preventative services, so most plans will include annual preventative screenings, and even a gym membership.

Generally, Advantage Plans have lower premiums than Supplement Plans. However, this is because you are agreeing to use Doctors who are in the plan’s local network, and you will pay copays when you visit Doctors and hospitals. Conversely, a Medicare Supplement Plan has no networks and little to no copays, depending on which Supplement Plan you choose.

The Government created the Medicare Advantage program over 20 years ago, in order to give Medicare beneficiaries a lower-premium option than Medigap. If you can’t afford a Medigap Plan, Medicare Advantage is your next best option in terms of coverage. Also these plans require very little underwriting, so if you missed you open enrollment period for Medigap and now you can’t qualify for Medigap due to health conditions, this is a good alternative option.

These plans are offered by private insurance companies, so when you enroll in an Advantage Plan, Medicare will pay the insurance company a fee every month to administer your Part A and B benefits. So you will need to enroll and remain enrolled into Medicare Parts A and B in order to have an Advantage Plan. The private insurance company that’s offering the Advantage Plan fully takes on the risk associated with your medical expenses. When you go to a Doctor or hospital, you will present your Advantage plan ID card, and your providers will bill the plan instead of Original Medicare.

What is the cost of an Advantage Plan

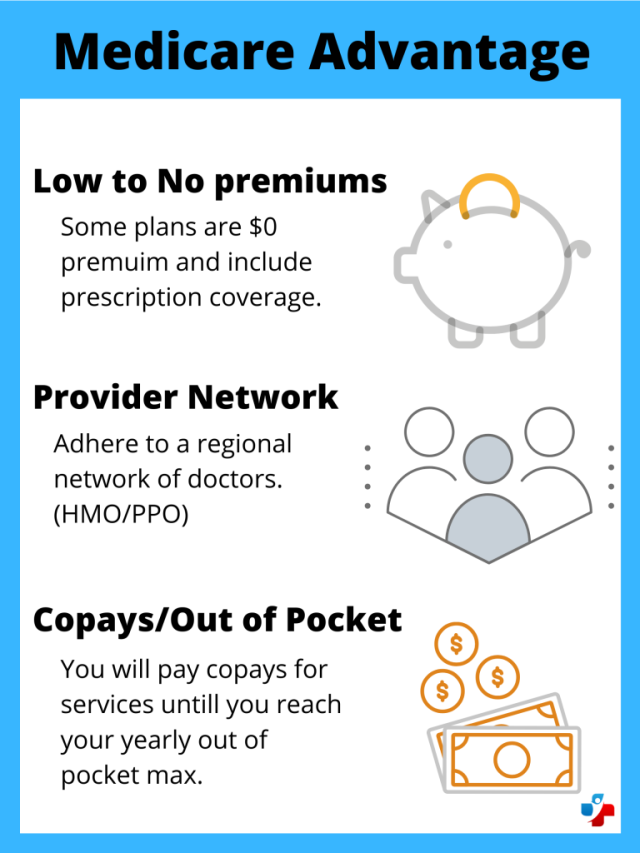

The monthly premium for a Medicare Part C Plan is usually much lower than the premium for a Supplement Plan. There are even several $0 premium plans that offer additional benefits such as hearing, dental, vision, preventative screenings, and gym memberships.

With an Advantage Plan you will usually pay copays when you visit Doctors and hospitals. However, most of the time a Medicare Part C Plan will have an out-of-pocket maximum. The only plans that may not have this feature are dual eligible plans for people with Medicare and Medicaid. The out-of-pocket max is an amount that is decided by Medicare each year. Currently, this number is $6,700. Depending on your location, there may be plans available with a lower out-of-pocket max cost. This can be a great value for some because Original Medicare has no out-of-pocket maximum. You are required to pay 20% of your services over and over again. With a Medicare Advantage Plan, you should just budget for the fact that you will have to pay copays for services (until you reach the out-of-pocket max). Every Advantage Plan has its own summary of benefits. This summary will tell you what your copays will be for various healthcare services.

Copay rates vary between states and counties, but average copays could be between $5-20 for Doctor’s visits, $40-$50 for Specialist’s visits, $250-$400 for surgeries, and $250-$350 per night for Hospital stays.

Medicare Advantage Enrollment Periods

There are a few time periods you can enroll into a Medicare Advantage Plan. The first enrollment period is your Initial Enrollment Period, which is when you turn 65. Once you enroll in Medicare Advantage, you must stay enrolled in the plan for the rest of the calendar year. After your Initial Enrollment Period passes, you can enroll or dis-enroll only during certain times of year. The next time you can enroll or dis-enroll from an Advantage plan is during the Annual Enrollment Period. This period runs from October 15th until December 7th each year.

The changes you make to your enrollment during this time will take effect January 1.

It is in your best interest to enroll in Medicare Advantage through an unbiased insurance agent, who can fully explain how the plan works. Enrolling without an agent means you are on your own if your run into problems with your policy, or don’t enroll correctly.

Why are Medicare Advantage plans free?

Many Medicare Advantage plans have a $0 premium, but this does not mean they’re free, you just pay for the plan in other ways than a premium payment. For one, you will still be paying the Part B premium to Medicare (and Medicare in turn pays the Advantage Plan insurance company to take on your medical risk). Also you will pay copays and possibly a deductible as you use your benefits. Copay and deductible amounts are plan specific, so you will be able to get those details when you are comparing plans with your insurance agent.

Medicare Advantage Networks (HMO and PPO)

A Medicare Advantage plan usually has networks. There are two main types of networks with an Advantage Plan, an HMO and a PPO. An HMO plan is where you will need to choose a primary care physician and get referrals to visit specialists. You do not have access to out of network Doctors in an HMO. You will only be able to access out of network providers in an emergency situation. With a PPO plan, you will have access to Doctors in and out of the provider’s network, and you will not need a referral to visit your specialist. Despite what some may tell you, a PPO plan still has networks. You will usually get charged more money for visiting an out-of-network Doctor. The only true no-network Plans are Medicare Supplement Plans.

Medicare Advantage versus Original Medicare

What is the difference between Original Medicare (Parts A and B) and Medicare Advantage (Part C)? With Original Medicare you will have deductibles to pay and a 20% coinsurance on Part B. However, you can go to any doctor or hospital that participates in Medicare, and most do.

With an Advantage plan, you will use the plan’s local network of providers. So you will want to make sure that your preferred Doctors are in the plan’s network before you enroll into an Advantage Plan. You will also pay co-payments when you receive healthcare services. However, you will not need to pay a coinsurance, and you will have an out of pocket maximum spend (which Original Medicare does not have). This caps your annual healthcare expenses at a certain amount.

Another big difference between Medicare Advantage and Original Medicare is in changes to the plans year over year. Original Medicare may have small changes to Part A and Part B deductibles, but that’s about the only change you should see. Medicare Advantage plans on the other hand change annually. An Advantage Plan’s premium, copayments, and networks could change. So it’s a good idea to review your Advantage Plan’s benefits annually. If you are no longer happy with your plan’s benefits you could make changes during the Annual Enrollment Period.

Need more help from the Medicare Experts?

Our well trained agents are ready to answer questions about your Medicare health insurance, and put together a comprehensive plan to fit your needs. Request more information by any of the 3 ways bellow!

Call Us

866-599-6588

Schedule Appointment

Request

A Quote

Medigap Insurance Carriers is not affiliated or endorsed by the United States Government or the Federal Medicare Program. This is a solicitation of insurance.

An agent/producer may contact you for insurance. Medigap Insurance Carriers is a DBA wholly owned by John Ross Anthony Webb.

©Copyright | Medigapinsurancecarriers 2022. All Right Reserved